WANT TO BUY OR SELL A PROPERTY?

CALL US TODAY · 808-298-8956

Real Estate Professionals With Mission Critical Results

This One Is For Our Veterans

By: Ethan Shelton

20 November 2022

- Boosting the VA guaranty to 60 percent of the loan amount, not to exceed $7,500

- Extending the maximum loan term to 30 years

- Providing access to the program to surviving spouses of veterans who died in service or as the result of a service-connected disability

- Authorizing the VA to create regulations governing the fees and costs lenders could charge to veteran homebuyers

- Four years later, Congress introduced a slate of updates and additions as part of the Veterans Housing Act of 1974. One of the biggest was the ability of veterans to restore their complete VA loan entitlement after selling a home or paying off the loan and disposing of the property. With one pen stroke, more than 4 million veterans suddenly regained the ability to obtain a new VA home loan

Some of the other notable changes contained in the 1974 act included:

- More lenders were now able to automatically process VA loans, provided they met department criteria.

- VA now had the power to approve condominium developments without previous action from the U.S. Department of Housing and Urban Development, better known as HUD

- Grant amounts for the specially adapted housing program increased to $25,000 from $17,500

- VA removed time frame restrictions regarding the purchase of manufactured homes

- Farm and business loans were removed from the program, leaving the focus solely on primary residences

- The guaranty level increased to $25,000 four years later. Energy efficient improvements also entered the picture in 1978. The VA would now guaranty loans that would improve a property with technologies like solar heating.

- Ensured the VA home loan program would be exempt from sequestration should it occur

- Required the government to use state data when determining residual income requirements

- Authorizing a three-year test of a VA adjustable-rate mortgage (ARM)

- Extending home loan eligibility to those who've served at least six years in the Reserves or National Guard

- Creating a program that allows veterans to add money to their mortgage for energy efficiency improvements

- Reducing to 0.5 percent the funding fee on VA Streamline refinance loans.

- Two years later, the VA decided it would provide a one-time restoration of entitlement for borrowers who pay off their loan but want to hold onto their home.

- New laws also expanded energy efficient mortgages (EEMs) into the Streamline program. In 1996, the government decided to make EEMs a permanent part of the loan guaranty program.

VA loan is a catch-all term for any mortgage loan that’s backed by the Department of Veterans Affairs, but that doesn’t mean all VA loans are the same. In fact, there are a few different types of VA loans, each of which is right for a different type of borrower. Check out this list to learn more:

VA purchase loan: A VA-backed purchase loan gives you the funding you need to purchase a primary residence (a home that you’ll be living in). With no down payment and lower interest rates, these loans can help veterans afford a home to live in.

VA renovation loan: VA renovation loans give you access to the money you need to repair or renovate a fixer-upper. This means that you can use a VA loan to purchase and fix up a home that ordinarily wouldn’t qualify for VA loan funding.

VA cash-out refinance: These loans let you replace your existing loan with a new one, plus you can get access to your home equity in the form of cash if you need quick cash. It’s important to consider your options before using a cash-out refinance.

VA interest rate reduction refinance: One of the common reasons to refinance is to lower the interest rate on your loan. With a VA interest rate reduction refinance, you can lower your interest rate so you aren’t paying as much for your mortgage.

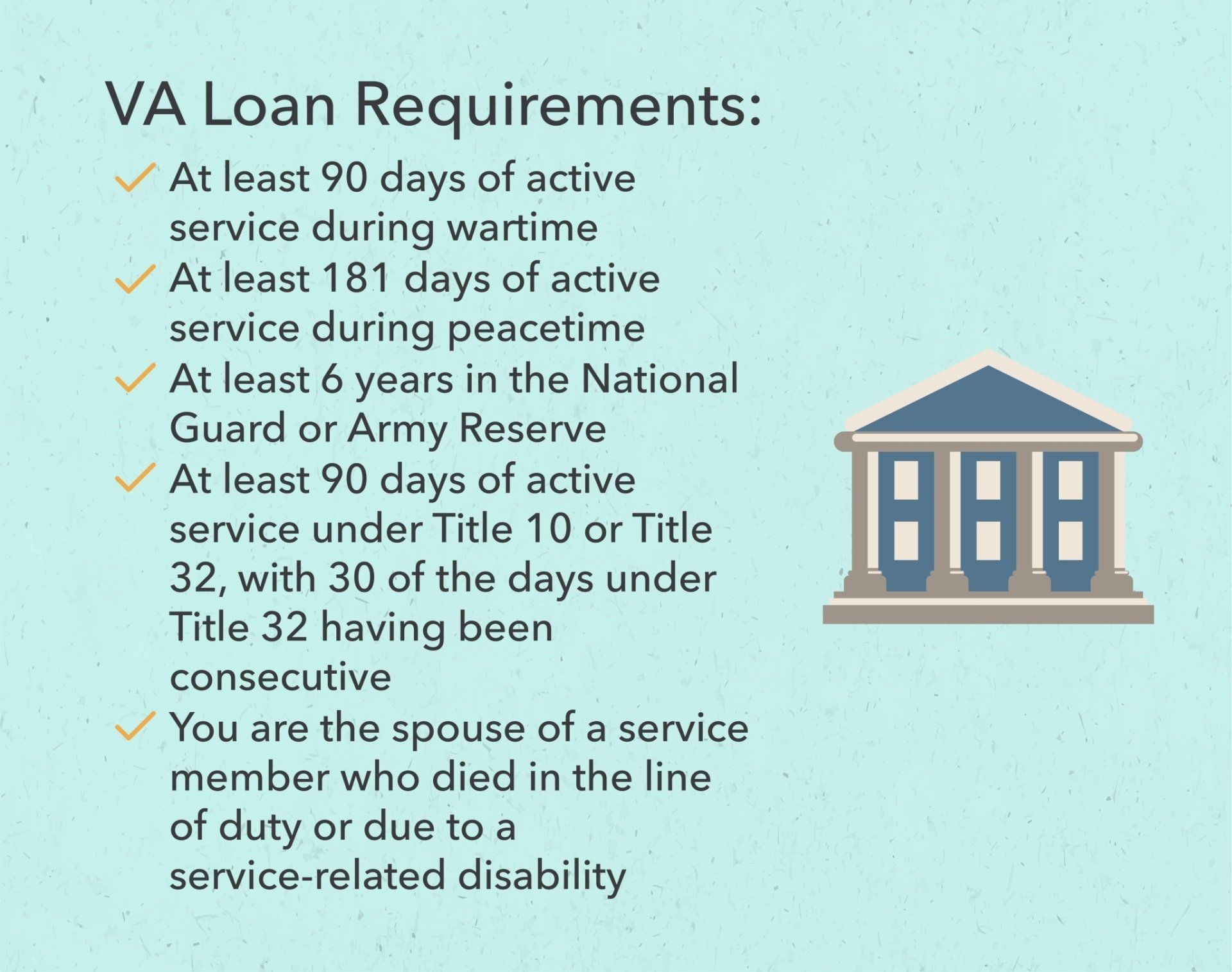

In order to qualify for a VA loan, you’ll need to meet certain VA home loan requirements. Individuals who apply for a VA loan will need to have a Certificate of Eligibility, which essentially tells the VA that you’re eligible for one of these loans. In order to qualify for VA loan eligibility, you must meet at least one of the following requirements:

- Have at least 90 days of service during wartime

- Have at least 181 days of service during peacetime

- Be a member of the National Guard or Army Reserve for at least 6 years

- Have at least 90 days of active service under Title 10 or Title 32; at least 30 days of your Title 32 service must be consecutive

- Be the spouse of a service member who died in the line of duty or as a result of a service-related disability

- Once you meet one of these VA loan requirements, you can obtain a Certificate of Eligibility to apply for a VA loan.

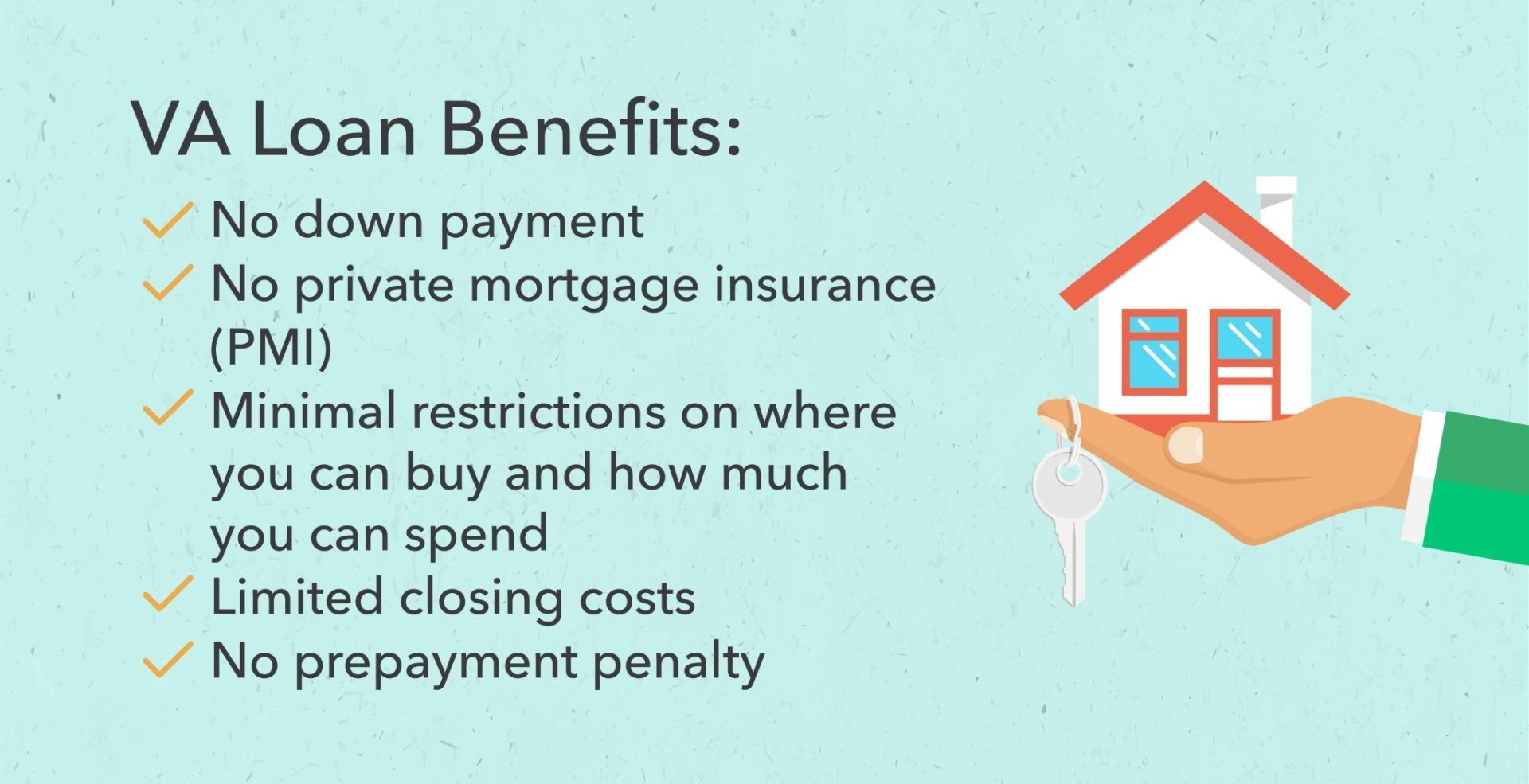

There are several potential benefits to applying for a VA home loan, including favorable loan terms and lower closing costs. Here are some of the biggest benefits you can enjoy from applying for a VA loan instead of a traditional mortgage loan:

- No down payment required

- No private mortgage insurance (PMI)

- Minimal restrictions in terms of where you can buy and what you can spend

- Limited closing costs

- No prepayment penalty

While there are lots of reasons you may want to apply for a VA loan, it’s important to keep in mind that all the basic rules of buying a home still apply. You may want to use an inflation calculator and look at real estate trends in the area to make sure you’re getting a good deal on the home you purchase.

Now that you know a little more about VA loans, you might be wondering how to apply for a VA loan. Just like a regular mortgage loan, there are certain steps you need to follow when it comes to applying for a VA loan and purchasing a home with a VA loan.

Obtain a Certificate of Eligibility (COE)

The first thing you need to do to apply for a VA loan is to obtain a Certificate of Eligibility. This certificate essentially proves that you’re eligible for a VA loan through one of the VA home loan requirements. You can apply for a Certificate of Eligibility online using the Department of Veterans Affairs e-Benefits portal, or you can have a loan officer request your COE electronically. You can also request a Certificate of Eligibility by mail using VA Form 26-1880.

Find a Lender

Now that you’ve got your Certificate of Eligibility and you know how to budget to buy a home, it’s time to find the right lender. You need to make sure you choose a lender who’s approved by the Department of Veterans Affairs, as these are the only lenders who can originate VA mortgages. You can also look for a lender who specializes in VA loans rather than offering them alongside traditional mortgages—that way you can find a lender who knows VA loans inside and out.

Get Pre-Approved

Once you’ve found a VA-approved lender and have your COE, you can get started with pre-approval. You don’t have to get pre-approved for a VA loan, but it’s a smart idea for most home buyers. Getting pre-approved lets you know how much money you have to spend so that you can start shopping for houses within your budget.

Find a Home

Now that you know how much money you have to spend on a home, you can start the shopping process. It’s a good idea to work with a real estate agent who specializes in VA loan transactions, that way you can make sure you’re getting the most out of your VA loan benefits.

Make an Offer

When you find a home you want to purchase, you can talk to your real estate agent about making an offer. This is one of the last steps in purchasing a home, so make sure you only make an offer on homes that you really want to purchase.

Undergo a VA Appraisal

Before you can actually buy a home, a VA appraiser will have to take a look at it. VA appraisers help you make sure you’re not paying too much for a home, which in turn helps lenders avoid loaning you money on a home you’re paying too much for. This is standard practice with any type of mortgage.

Close on Your Home

Once all the previous steps have been completed and your offer has been accepted, you can close on your home. VA loans often come with lower closing costs, and you may or may not need to worry about having private mortgage insurance. During the closing process, it’s important to talk with your real estate agent about what you need to do as a buyer.

Final Notes

Since 1973 we have had an all volunteer military and for whatever reason that compelled our young Americans to take up arms, we did it knowing it could be a one way trip and for thousands it was. There are many that say they do not like the direction the Unites States is going but because of the Brave we have the choice in what the "Home of the Free" looks like.

Securing a VA loan can be a good way for veterans to purchase a home, but know this. They are exclusively for veterans on behalf of a grateful nation.

Please take a moment to watch this video from Mark Connors of Veterans Affairs share his thoughts of the Veterans Home Loan Program.

No matter which branch of the service you served in, you are all my brothers and sisters and have my deepest gratitude and respect. Thank you all and may God Almighty bless you and keep you whole.

Contact Us

LOCATION

214 Hooulu Lane #305

Wailuku, Hawaii 96793

BOOTS ON THE GROUND

Consider Ascentia Maui to be your resource for all Real Estate Needs with a heavy emphasis on Probate, Trusts, Conservatorships and Guardianship Sales. You can also count on Ascentia Maui as your 'Boots on the Ground' for Cleaning, Lawn service Surveys, Inspections, Contractors or anything you may need.

CONTACT US

ascentia Maui, LLC is an organization that operates under the brokerage licensing of Keller Williams Realty Maui. Paragraph

285 W. Kaahumanu ave. #201 Kahului, Hawaii 967362w

Each office is independently owned and operatedParagraph