WANT TO BUY OR SELL A PROPERTY?

CALL US TODAY · 808-298-8956

Real Estate Professionals With Mission Critical Results

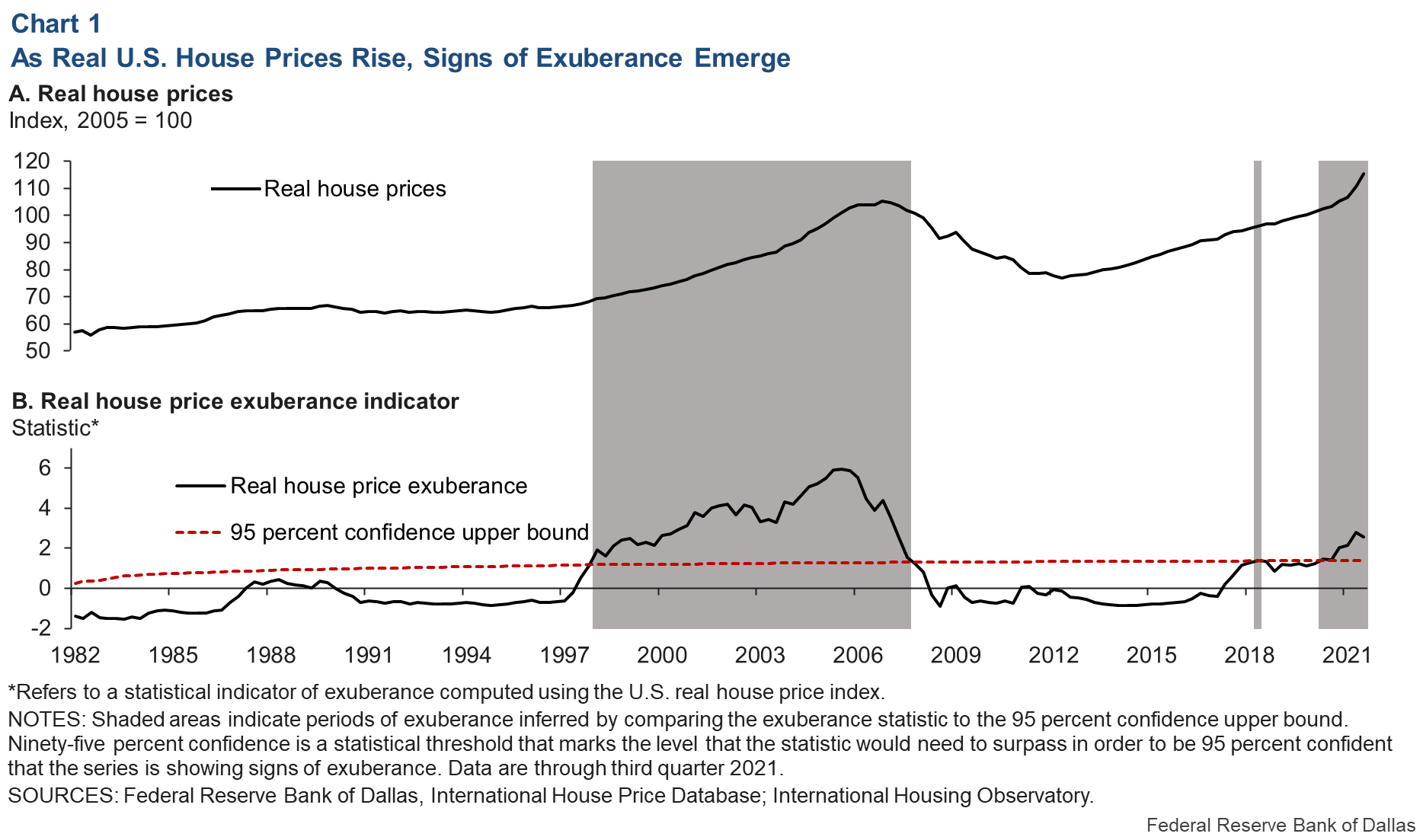

Real-Time Market Monitoring Finds Signs of Brewing U.S. Housing Bubble

The U.S. is not alone in experiencing housing market fever. Eleven of the 25 countries in the Dallas Fed’s International House Price Database show signs of real house-price exuberance.

A Diagnostic Approach to U.S. Housing Markets

To assess U.S. house prices during the pandemic, we first develop an empirical relationship between house prices and those economic fundamentals underpinning the market, based on data through fourth quarter 2019. The theoretical benchmark is the fundamental value of housing based on the sum of discounted future rents. (see earlier posts for more on rent correlation)This is similar to the finance tenet that the fundamental value of a company’s stock is the flow of future dividends discounted by the cost of capital. (Analogously, the company here is a house, and its dividends are rents that are discounted by interest rates.)

Working from that benchmark, the house-price-to-rent ratio is explained by a small set of lagged economic variables, such as personal disposable income per capita, housing rents and long-term interest rates. The residual of the regression, after removing the effects of fundamentals, is assessed for any remaining evidence of explosive behavior. The upshot: Since the beginning of 2020, the price-to-rent ratio has soared beyond what observed fundamentals alone can explain (Chart 2).

The gap between the actual price-to-rent ratio and its fundamental-based level in the U.S. has grown rapidly during the pandemic—comparable to the run-up of the last housing boom—and started showing signs of exuberance in 2021. The exuberance statistic confirms that recent increases are far from ordinary.

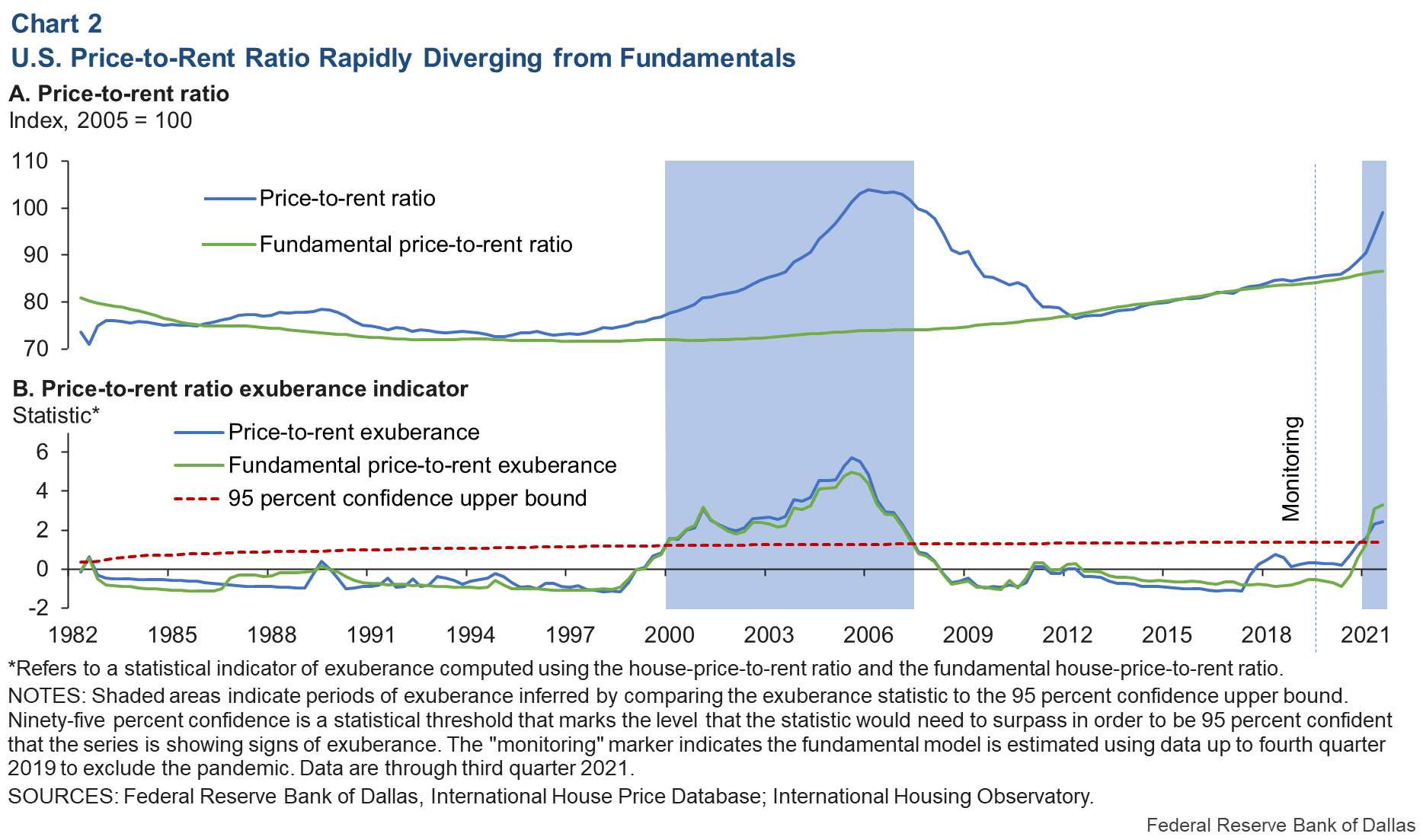

Another important long-run anchor—tied directly to housing affordability—is the ratio of house prices to disposable income. Chart 3 shows dates of episodes of exuberance for this measure of housing affordability. These data—unlike our previous metrics—do not yet display evidence of explosiveness in the third quarter of 2021. But the rapid increase in the statistic close to the threshold during 2021 indicates that U.S. real house prices may soon become untethered from personal disposable income per capita.

The delay in elevation of this exuberance statistic is partly the consequence of a surge in real disposable income during the pandemic that led to slower growth rates in the price-to-income ratio. The surge in disposable income is mostly associated with pandemic-related fiscal and monetary stimulus efforts and reduced household consumption arising from mobility restrictions and lockdowns.

If disposable income increases turn out to be transitory—as fiscal stimulus wanes and the Federal Reserve reverses its accommodative monetary policy (goodbye q.e.)—recent patterns in the price-to-income ratio may prove a less-useful measure of housing affordability. Such transitory increases in disposable income are not strong determinants of long-term housing investment. Thus, the price-to-income ratio measure alone may produce overly conservative results when identifying housing market bubbles.

Another U.S. Housing Bubble Brewing?

Our evidence points to abnormal U.S. housing market behavior for the first time since the boom of the early 2000s. Reasons for concern are clear in certain economic indicators—the price-to-rent ratio, in particular, and the price-to-income ratio—which show signs that 2021 house prices appear increasingly out of step with fundamentals.

While historically low interest rates are a factor, they do not fully explain housing market developments. Other drivers have played a role, including pandemic-related U.S. fiscal stimulus programs and COVID-19-related supply-chain disruptions and associated policy responses. The resulting fundamental-driven higher house prices may have fueled a fear-of-missing-out wave of exuberance involving new investors and more aggressive speculation among existing investors.

Based on present evidence, there is no expectation that fallout from a housing correction would be comparable to the 2007–09 Global Financial Crisis in terms of magnitude or macroeconomic gravity. Among other things, household balance sheets appear in better shape, and excessive borrowing doesn’t appear to be fueling the housing market boom.

Importantly, experience from the housing bubble in the early 2000s and the subsequent development of advanced tools for early detection and deployment of warning indicators—some illustrated in this analysis—mean that market participants, banks, policymakers and regulators are all better equipped to assess in real time the significance of a housing boom. Thus, they are in a more-informed position to react quickly and avoid the most severe, negative consequences of a housing correction, at least one would hope so.

LOCATION

214 Hooulu Lane #305

Wailuku, Hawaii 96793

BOOTS ON THE GROUND

Consider Ascentia Maui to be your resource for all Real Estate Needs with a heavy emphasis on Probate, Trusts, Conservatorships and Guardianship Sales. You can also count on Ascentia Maui as your 'Boots on the Ground' for Cleaning, Lawn service Surveys, Inspections, Contractors or anything you may need.

CONTACT US

ascentia Maui, LLC is an organization that operates under the brokerage licensing of Keller Williams Realty Maui. Paragraph

285 W. Kaahumanu ave. #201 Kahului, Hawaii 967362w

Each office is independently owned and operatedParagraph