WANT TO BUY OR SELL A PROPERTY?

CALL US TODAY · 808-298-8956

Real Estate Professionals With Mission Critical Results

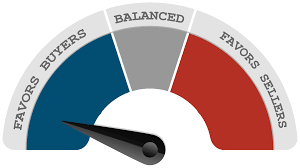

Buyers Market With Sellers Metrix?

Created: Nov 5, 2022

By: Ethan Shelton

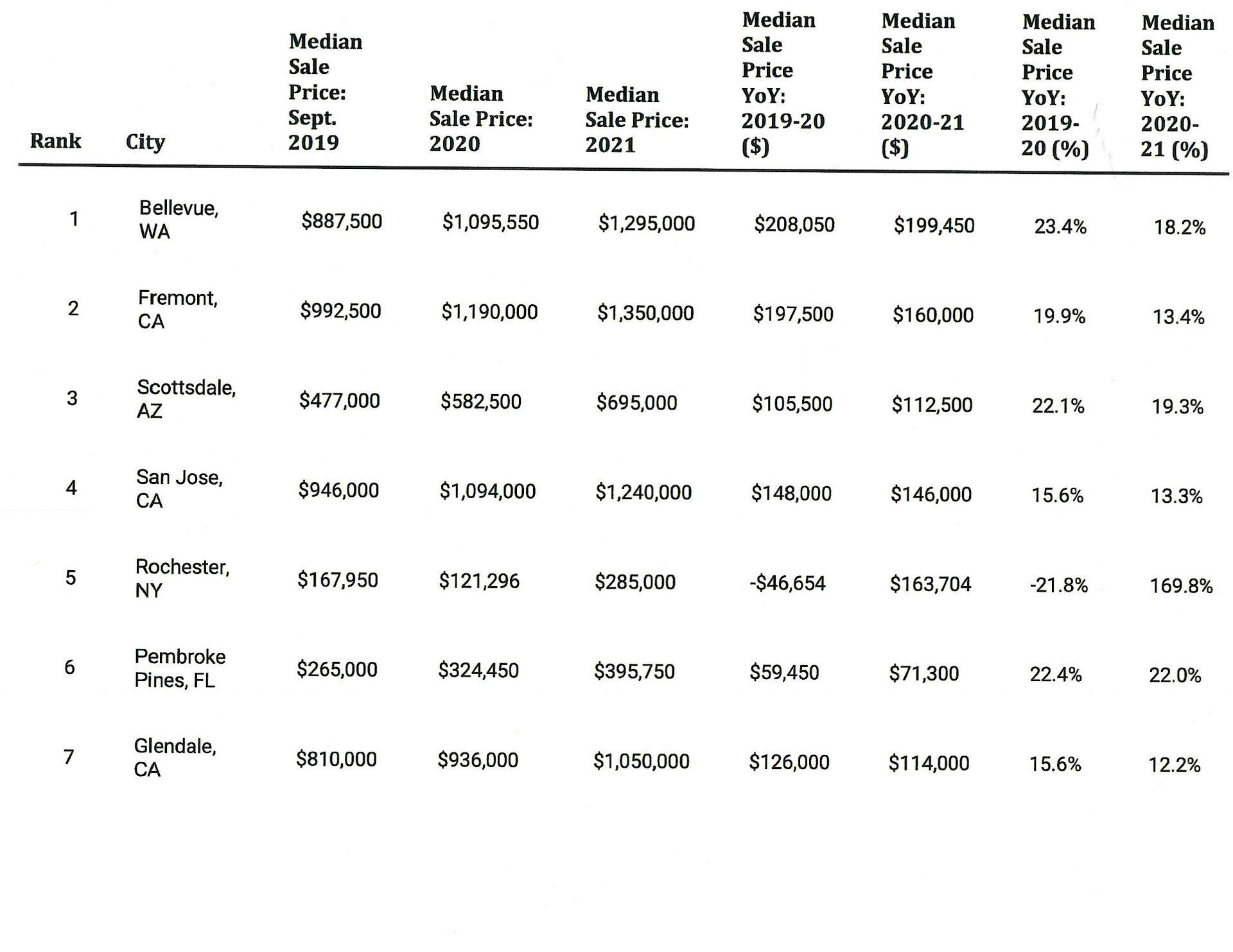

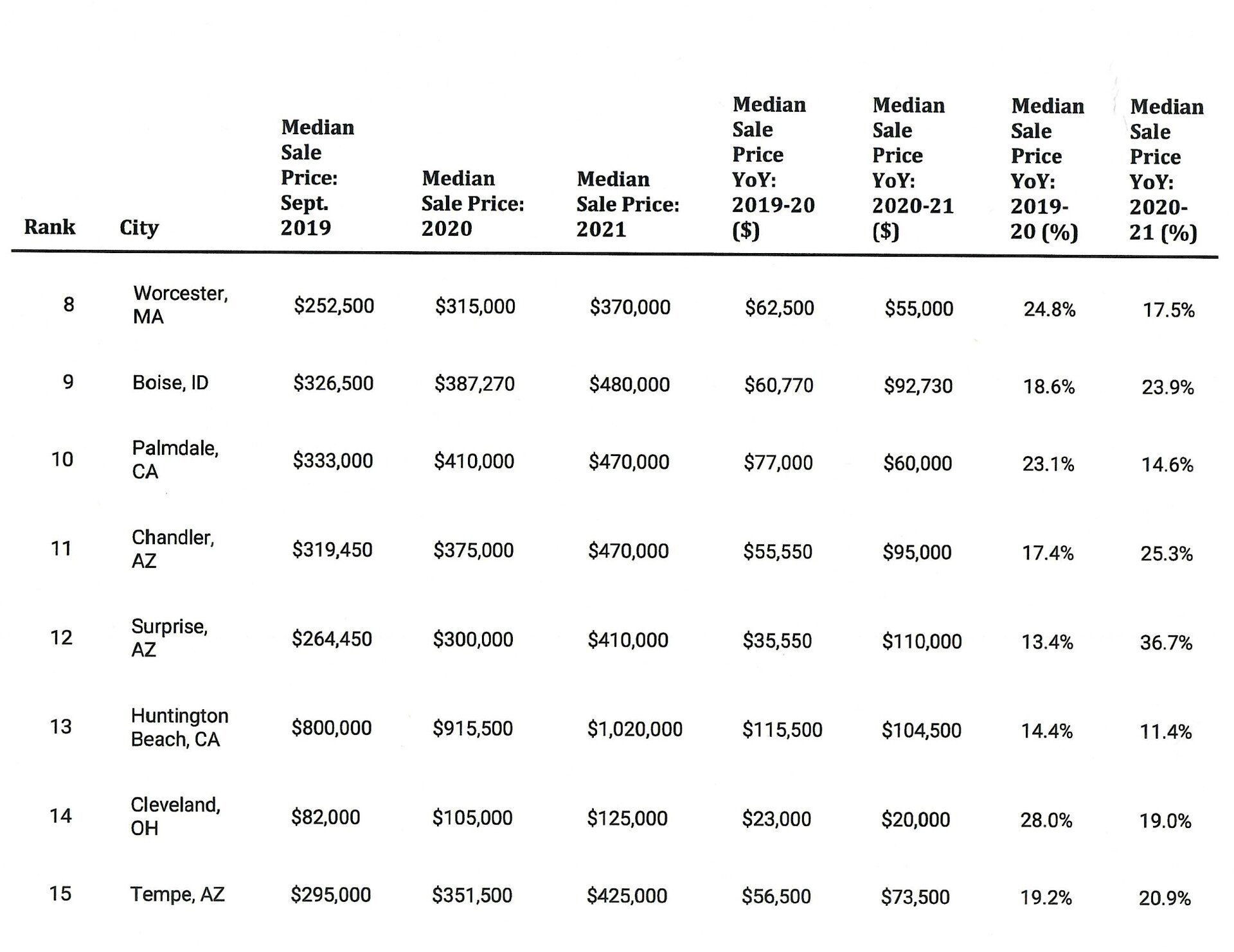

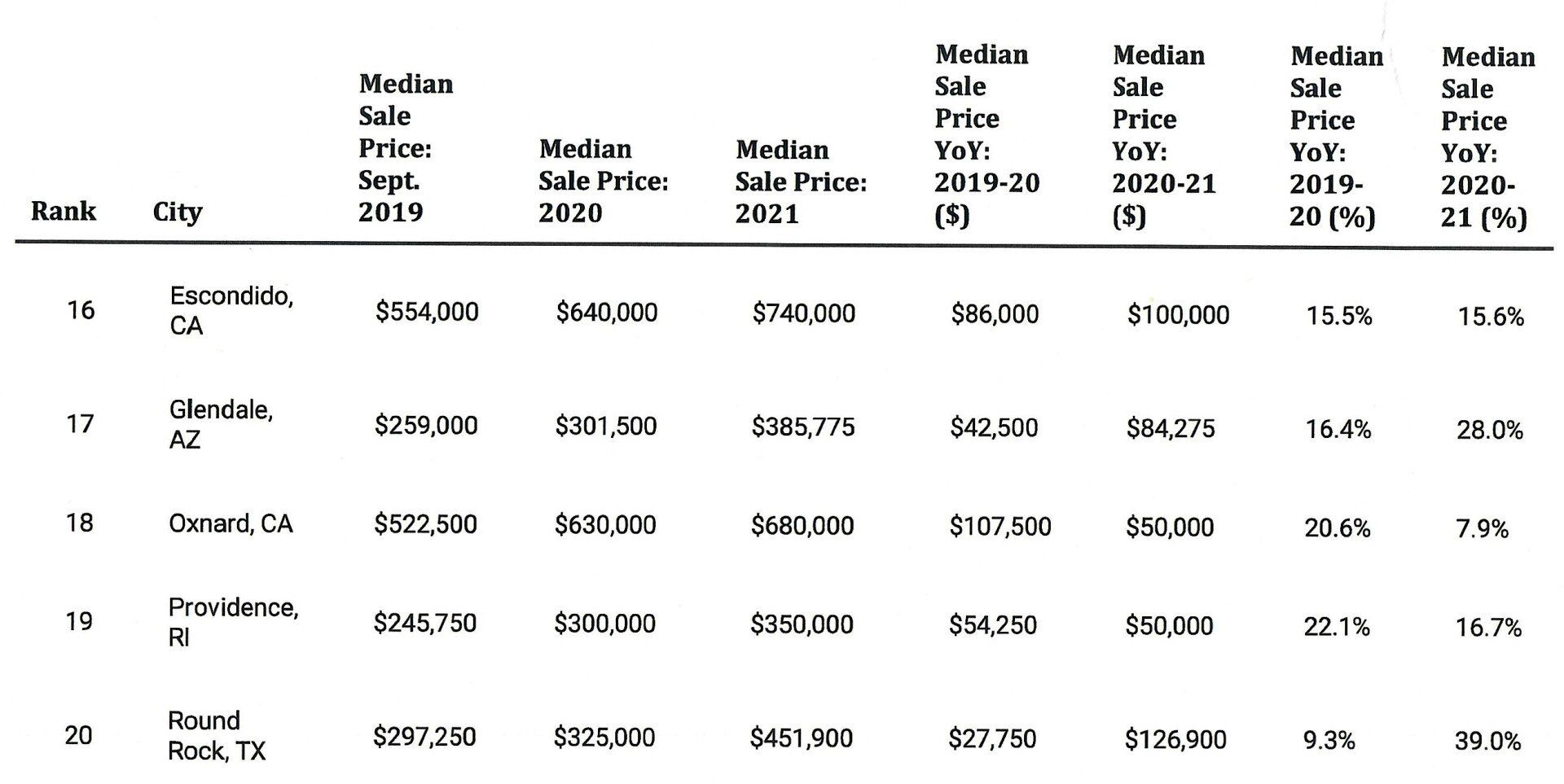

Looking at the slightly crooked graph below we would be inclined to believe everyone selling their home is getting asking price or even more however that isn't the whole story. A quick look at the MLS shows us that behind the scenes realtors have their way of skewing numbers (although not their fault). Realtors Association of Maui only reports the final numbers to the consumer but doesn't reflect the record number of price "Improvements" or price drops. In the last 30 days alone we saw 133 new listings and 107 price drops.

In the 90's it wasn't uncommon for homes to be on the market for 6 to 8 months and longer. you didn't really find that with those that were still making large mortgage payments though. a year of making payments can put a real dent in your net proceeds at the close of escrow.

Moving forward, Realtors will want to adjust their pricing strategy to reflect a more apprehensive market.

Here is what it looks like across the pond

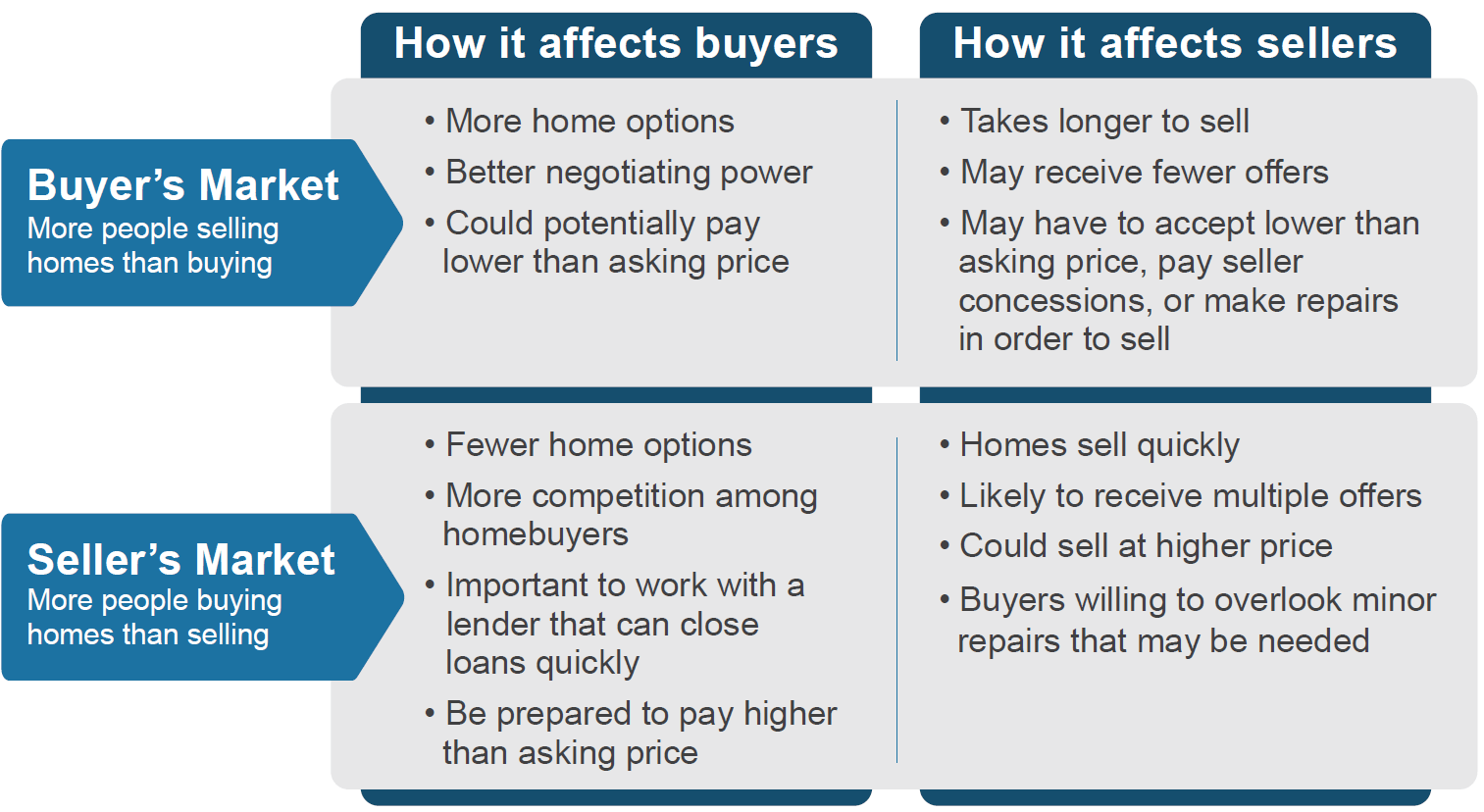

Signs you’re in a buyer's market

Anyone who’s shopped for a home in the last few years knows what a seller’s market looks like. Listings are few and far between. Homes sell at lightning speed. And when you do find a great place, you’re up against a dozen other buyers — forced to outdo and outspend.

Buyer's markets are just the opposite. Instead, supply outweighs demand, giving home shoppers the upper hand both when hunting for a home and when negotiating for it.

Sellers offer more incentives, such as [contributing to buyers’] closing costs, and are willing to take more contingencies than in the past, Additionally, Homes take longer to sell, and [price] appreciation slows or even drops a little.

San Francisco is case in point. In August, it took 24 days for the typical San Fran home to sell, double the time seen last year. Home prices have also slipped steadily since May and are now down 5% compared to last August.

If you’re not seeing similar happenings in your market just yet, don’t fret. Pros say the shift from a seller’s market to a buyer's one is usually gradual. Conditions change incrementally, and eventually, the market flips.

The Good News for buyers is

The silver lining for buyers is less competition. higher mortgage rates which have shrunk affordability significantly in recent months are whittling down the competition just about everywhere. “The rapid rise in interest rates has sharply reduced the number of potential homebuyers,” says Cristin DeRitis, deputy chief economist at Moody’s Analytics.

That’s a great thing if you’re still on the house hunt, as it means fewer bidding wars and less feverish negotiations. You probably won’t need to bid way over asking price or waive vital contingencies which allow you to back out due to home inspection findings, a low appraisal or your loan falling through just to get noticed.

“The demand frenzy witnessed in the first two quarters of 2022 is no longer,” says Karen Kostiw, an agent with Coldwell Banker Warburg. “Sellers are no longer demanding that buyers eliminate contingency clauses from the contract.”

Strategies for buying right now

Buyers shopping in today’s changing market will likely have more leverage than they’re used to, but conditions won’t be perfect. Fortunately, there are a few strategies that can help ensure success.

First, don’t feel pressured to make snap decisions but, do act with some level of urgency. While bidding wars are probably not going to be the norm in most areas, you can still expect to face competition.

Let's just call it like it is

I was thinking that instead of trying to put a round peg in a square hole, we would just avoid generalization altogether and just acknowledge we are in a higher interest rate environment which by design has put a screeching halt on inflation in several sectors of the economy and real estate has been the first to react.

In a higher interest environment the only real consideration is affordability for someone that needs a place to live so let's take a brief look at how we helped people own homes before the gravy train arrived in 2020.

A few financing nuggets

First, You may be able make more demands than you could have a few months ago, like including contingencies or asking the seller to contribute to your closing costs.

If today’s 7.86% mortgage rate is challenging your budget, you can also ask the seller to buy down your interest rate, essentially making a lump-sum payment to your lender, reducing your interest rate (and payment) for the first few years of the loan.

Assumable Loans

A recent survey commissioned by bankrate and conducted by Yougov showed that 74% of mortgage holders did not refinance when they had the chance in 2020 stating largely that after closing costs and fees, it wasn't worth the savings. It was a stark contrast to the people that took advantage of declining rates sometimes refinancing several times.

That could mean some very good news for the would be homeowner that finds their plans put on hold until rates come down. An assumable loan or mortgage is a very viable option to breathe new life into a home search.

"Mortgage assumption is the conveyance of the terms and balance of an existing mortgage to the purchaser of a financed property, commonly requiring that the assuming party is qualified under lender or guarantor guidelines." wikipedia

Not all mortgages are assumable but there are a few that are and they are numerous. FHA has helped millions of people finance their homes, usually at lower rates than conventional loans and while you still have to qualify, they are very much assumable.

U.S. Department of Veterans Affairs (VA) were introduced in 1944 as part of the GI Bill of Rights Act to ease the transition from military to civilian life. They come with a long list of benefits like no down payment requirements and lower interest rates. While these loans are designed for veterans and they will get first priority, they are also assumable.

U.S. Department of Agriculture (USDA) A USDA loan is a government-backed, no money down mortgage with government-assisted mortgage rates, which means you can get lower rates than with similar government-backed programs like FHA and VA and although it’s the government agency best known for its work with farming, forestry, and food, it also does work in housing.

Since USDA loans don’t require a down payment, you can borrow as little or as much as you need to buy a home – as long as that home is in a “rural,” or less densely populated, area.

Rural areas might include the outskirts of town, a place with lots of farmland, or a suburb of a large city — really anywhere that’s not considered “urban.”

Wraparound Mortgage

A wraparound mortgage, more commonly known as a "wrap", is a form of secondary financing for the purchase of real property. The seller extends to the buyer a junior mortgage which wraps around and exists in addition to any superior mortgages already secured by the property.

example: Both Michaela and Alex agree to a $10,000 down payment and $150,000 wrap-around mortgage from the seller at a 6% fixed interest rate. Alex pays Michaela monthly for the second mortgage, which Michaela uses to pay off her original mortgage and keeps the difference between the two payments.

Final Thoughts

There is little doubt the economic environment is changing and buying a home just became a bit more challenging but that doesn't mean hope is lost. in fact far from it. there is a reservoir of untapped possibilities in the secondary market just waiting for a determined homeowner that doesn't mind an extra step or two to put a roof over their family's head.

Now get out there and find you a

realtor with grey hair

that remembers how to put these deals together and let's keep the American dream of homeownership alive.

Contact Us

LOCATION

214 Hooulu Lane #305

Wailuku, Hawaii 96793

BOOTS ON THE GROUND

Consider Ascentia Maui to be your resource for all Real Estate Needs with a heavy emphasis on Probate, Trusts, Conservatorships and Guardianship Sales. You can also count on Ascentia Maui as your 'Boots on the Ground' for Cleaning, Lawn service Surveys, Inspections, Contractors or anything you may need.

CONTACT US

ascentia Maui, LLC is an organization that operates under the brokerage licensing of Keller Williams Realty Maui. Paragraph

285 W. Kaahumanu ave. #201 Kahului, Hawaii 967362w

Each office is independently owned and operatedParagraph